In 1991 Billy and Akaisha Kaderli retired at the age

of 38. Now, into their 4th decade of this

financially independent lifestyle, they invite you

to take advantage of their wisdom and experience.

The S&P 500 finished the week at 7,411.98, down about 0.6%, as an AI capex scare

and an oil shock collided into its second straight weekly decline and the first

back-to-back down weeks since March. The headline number hides what actually

happened. Underneath a falling index, the average stock held up just fine.

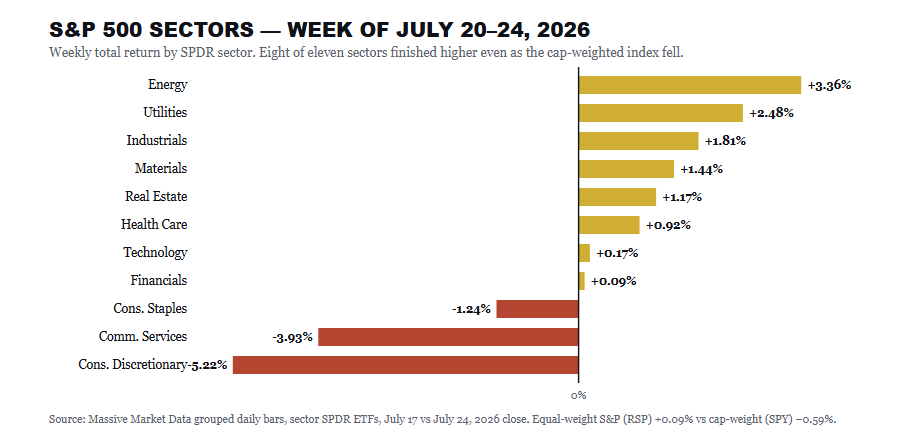

Eight of the eleven S&P sectors rose on the week. Energy led, up 3.4% as crude

spiked, and the more defensive and cyclical corners of the market, utilities,

industrials, materials, and real estate, all gained ground. Equal-weight RSP

actually finished higher, up 0.09%, while the cap-weighted SPY fell 0.59%. That

gap tells the story. The damage was surgical, concentrated in exactly two

places: communication services, down 3.9%, and consumer discretionary, down

5.2%. Those are the buckets that hold Alphabet, Meta, Amazon, and Tesla.

Thursday was the event. The Magnificent Seven shed roughly $800 billion in a

single session, the worst megacap day since the April 2025 tariff shock. The

triggers were Alphabet raising its capital spending plans again and Tesla’s

profit sinking. As we warned in Momentum

Meltdown Catches Traders By Surprise, the market’s narrow

leadership was always the biggest risk to the tape. This week, the generals took

the hit while the troops did not. The Nasdaq Composite lost about 2% on the

week, the worst of the major averages, while the Dow and the small-cap Russell

2000 barely budged.

Two other forces pressed on stocks. Oil surged with Brent briefly tagging $100

for the first time since May on fresh attacks in the Red Sea. WTI booked its

biggest weekly gain in months even after slipping to about $89.57 on Friday.

Rising crude prices pushed the 10-year Treasury yield up to 4.67% midweek before

easing on Friday as oil retreated. A new round of tariffs also took effect, but

none of them triggered panic. The VIX rose about 12% on the week but still

closed under 20, near 18.6.

So we head into a loaded week with the index below its 50-day moving average,

the momentum names wobbling, and breadth quietly improving. The question is

whether that broadening is the rally getting healthier or the last leg before

the leaders drag everything lower.

📈Technical

Backdrop–

Below The 50-Day, Testing Support

The S&P 500 spent most of the year riding above its 50-day moving average, and

we have warned for the last couple of weeks that a break lower would be worth

paying attention to. That break occurred on Thursday, as the index closed the

week at 7,411.98, roughly 0.8% below the 50-DMA at 7,467, marking its first

decisive break below that line in months.

Momentum has clearly rolled over. The 14-day RSI sits in the mid-40s, below the

neutral 50 line but not yet oversold, suggesting there is room for further

downside before the tape gets stretched. The MACD agrees with the signal line

crossing bearish about a week ago, and the histogram keeps widening to the

downside. This is what the early innings of a pullback look like, not the middle

or the end.

One encouraging detail sits beneath the surface. The tight link between the

hyperscalers and the semiconductors has broken down, and the chip complex

actually held up on the week, even as the megacaps were sold. Decliners still

outran advancers by roughly three to one on the New York Stock Exchange during

Thursday’s rout. This was a real risk-off session, not a quiet drift. A theme

that rotates internally behaves very differently from one that investors are

abandoning wholesale.

The bigger trend is still intact. The 200-day moving average sits at 7,001, and

the index remains almost 6% above it. A slide to the 50-DMA or even the July

closing low near 7,354 would be entirely normal inside an ongoing uptrend. The

line that matters is the 200-DMA. Lose that, and the conversation changes.

In our own models, we continue to hold the AI complex at target weight rather

than above it. We are not adding to them, given next week’s hyperscaler prints;

instead, we would rather let the reports clear and buy confirmation than pay up

for a guess. That discipline has kept risk contained through every one of this

year’s AI-driven air pockets.

Here is the setup for next week. First resistance is the 50-DMA at 7,467, then

the early-July high near 7,566, and the record close at 7,612. On the downside,

watch 7,354, then the June closing low at 7,266, and the 100-day average at

7,172. A close back above the 50-DMA would repair most of the technical damage.

A close below 7,266 would put the 200-DMA in play and argue for a more defensive

posture.

🔑 Key

Catalysts Next Week

Next week is the most consequential stretch of the summer. The Federal Reserve

makes its decision on Wednesday, and four of the five largest companies in the

index report within about 48 hours of that decision.

Start with the Fed. The FOMC

meets July 28 and 29, with the decision at 2:00 p.m. Eastern on

Wednesday and Chair Warsh’s press conference at 2:30. There is no new dot plot

at this meeting, so the statement language and the press conference are the

whole show. The funds rate has held at 3.50 to 3.75% all year on sticky

inflation. This week’s oil spike does not make the case for a cut any easier.

Watch how Warsh frames the inflation risk coming from energy.

Then the earnings deluge. Microsoft and Meta report on Wednesday after the

close, and Apple and Amazon follow on Thursday after the close. FactSet has S&P

500 earnings growing about 24.7% in the second quarter, marking the second

straight quarter above 20%. The bar is high, and the market’s patience is thin.

Companies that have missed this season were punished harder than usual, falling

an average of 4.2% against a historical norm closer to 2.9Z%.

The macro calendar fills in around those events. Consumer Confidence and

home-price data land on Tuesday. The advance reading of second-quarter GDP and

the June PCE deflator, the Fed’s preferred inflation gauge, both print Thursday

morning at 8:30. That lands right on top of the Apple and Amazon reports that

evening. Friday brings the Employment Cost Index and the final read on consumer

sentiment. There is no monthly jobs report this week, so the Fed and the megacap

prints will set the tone on their own.

For portfolios, the sequencing matters more than any single release. Wednesday

afternoon delivers the Fed plus Microsoft and Meta. Thursday delivers growth,

inflation, and the other two megacaps. By Friday’s close, we will know whether

the AI capex trade can absorb both a cautious Fed and its own cash-flow math.

Position sizes should reflect that this is a week built for surprises.

The AI

Capex Bill Comes Due

On Friday, I laid out the accounting catch hiding inside this year’s record

earnings in AI

Capex Depreciation Risk Is The Catch To Record Earnings. The

short version is simple. The AI capex boom has flattered reported profits while

quietly draining cash, and next week, four of the five biggest spenders report

at once. This is where the theory meets the tape.

The five biggest hyperscalers are on track to spend north of $725 billion on

capital projects in 2026, up from roughly $412 billion last year. Yet only about

$211 billion of that will show up as depreciation on 2026 income statements. The

rest, more than half a trillion dollars, sits on the balance sheet as a

long-lived asset and gets expensed over the years ahead. That timing gap is why

earnings can grow more than 20 percent while the cash going out the door

explodes higher. The

capex is REAL.

There is nothing improper about any of this. It is how companies book capital

assets, and it always works this way. What is different this cycle is the sheer

scale of the spending and the speed at which the deferred bill will land. As

Todd Castagno at Morgan Stanley put it, this is“a

golden window where everybody looks good.” The window does not stay

open forever.

Free Cash

Flow Is Draining, Not Disappearing

Here is where investors get the story half right. Depreciation

is a non-cash charge.It

lowers reported earnings, but it does not touch the cash a business actually

generates from operations. So when you watch a hyperscaler’s free cash

flow collapse, you are mostly watching capital spending outrun everything else,

not a business falling apart.

Amazon is the clearest example. Its trailing free cash flow fell to $1.2 billion

from $25.9 billion a year earlier. That looks alarming until you remember why.

The company is pouring roughly $200 billion into data centers, chips, and power.

Cash leaves today, and the asset it buys is designed to produce revenue for

years.

The mistake is treating compressed free cash flow as automatic evidence of

waste. Falling FCF

is far more defensible when it funds reinvestment than when it funds buybacks. Betting

on permanent cash-flow impairment is a bet against the best capital allocators

of the past two decades.

Negative free

cash flow tells you a company is spending. It does not tell you whether the

spending is smart. That answer shows up later, in the revenue the assets

produce.

The honest caveat is that a GPU is not a railroad. If the useful life of these

assets turns out shorter than management assumes, the depreciation bill arrives

faster, and the payback window compresses. That is the real debate, and it

deserves to be settled company by company rather than with a single scary

headline.

Four

Companies, Four Different Bills

Four of the biggest AI spenders report next week, and they sit in very different

places on this map. Microsoft reports on Wednesday with consensus at $4.22. It

is spending heavily, roughly $190 billion in calendar 2026, and the strain

already shows. Free cash flow fell to $15.8 billion last quarter on $31.9

billion of capex, down from $25.7 billion two quarters earlier. The

number that justifies the bill is Azure, which management guided to 39%-40%

growth. Hold that line, and the spend looks bought. Miss it, and the

cash-flow math gets uncomfortable in a hurry.

Amazon reports Thursday with consensus at $1.82. Its story is the same shape,

only larger. The roughly $200 billion capex plan drove trailing free cash flow

down to that $1.2 billion figure. But

AWS reaccelerated to 28% growth last quarter, its fastest in over three years,

with a backlog north of $360 billion, and is the entire tell. If cloud

growth holds, the buildout is converting. If it stalls, the market will ask much

harder questions about the check Amazon wrote. It did exactly that when the

stock fell 8% after the spending plan was first announced.

Meta also reports on Wednesday, with a consensus at $7.23, and it is the odd one

out. Meta is pouring a comparable fortune into AI, with 2026 capex guidance just

raised to $125 billion to $145 billion, yet it has no cloud division to sell

that capacity to (which

is why we don’t own it).

For Meta, the payback has to show up inside its own business, in sharper ad

targeting and deeper engagement, with Reality Labs and the new Meta Compute

effort as longer-dated options. That makes Meta the purest test of the four. Its

operating margin has already slipped from the peak as spending ramps up, and

free cash flow could turn negative if capex keeps climbing. Watch

whether AI is visibly lifting ad revenue. If it is, the spend defends itself. If

not, Meta has the least coverage in the group.

Apple is the counterexample, and that is exactly why it belongs here. It reports

Thursday with a consensus at $1.89, and it is barely part of this story. Apple’s

capital spending is a fraction of its cash generation, and it still throws off

enormous free cash flow every quarter. Its risks live somewhere else

entirely, in the iPhone upgrade cycle, Services growth, China, and the

perception that it has fallen behind on AI. This is also Tim Cook’s final

earnings call before John Ternus takes over, which adds a layer of narrative

that the numbers will not capture. Apple is the reminder that not every megacap

is running the same capex gauntlet, a point we made in Mag

7 Stocks: Risk Or Opportunity.

The Market

Is Treating The AI Capex As Dead Money

Watch how the tape reacted this month, and you’d think the AI buildout had

already failed. Alphabet

beat on revenue, grew Google Cloud 82%, and still fell about 5% after hours

because it raised capital spending again. As I posted on Thursday:

Amazon got the same treatment earlier this year. The market is pricing the bill

and ignoring the asset. That is usually where opportunity hides.

Be honest about the near-term risk first. Valuations are not cheap. The broad

market still trades well above its long-term average multiple, and the megacaps

carry a premium on top of that. Free cash flow is under real pressure, and

Alphabet just posted negative free cash flow of $5.9 billion and paused buybacks

to fund the buildout. Capex guidance keeps getting revised higher, not lower,

which means the deferred depreciation bill I described earlier is still growing.

Add a tape below its 50-day average and the worst three-month stretch of the

calendar dead ahead. More downside over the next quarter or two would not

surprise me.

The AI Capex depreciation risk is great for bearish headlines, clicks, and

views. However, it misses a critical point. Negative free cash for a company

that is losing market share, has declining revenue growth, and is unprofitable

is a clear investment risk.

However, that is not the story of the hyperscalers. The

revenue that justifies all this spending is accelerating, not fading. As

noted, Google Cloud grew 82%, Azure is running near 40%, and AWS reaccelerated

to 28%. The committed backlogs behind them are enormous, at $514 billion for

Google, north of $600 billion for Microsoft, and more than $360 billion for

Amazon. Those are

not the numbers of a dying business. They are the numbers of businesses that

cannot build capacity fast enough to meet demand.

This is where Howard Marks and his second-level thinking earn their keep. The

easy call is to sell what just went down. The harder and usually more profitable

call is to buy durable franchises when the crowd has decided the story is over. The

hyperscalers are not dead. They are expensive, early in the payback, and briefly

out of favor, which is a very different thing. We’d use this weakness to build

positions in the names where cloud growth and backlog clearly justify the spend.

And we’d do it in pieces rather than all at once.

What Should

Investors Do Now

None of this argues for abandoning the AI trade. It argues for pricing it

honestly. The businesses are real, the revenue is growing, and the best

operators have earned some benefit of the doubt. But valuations already assume

the capex converts cleanly, and next week, four companies have to show their

work. Here is how we are approaching it.

A number that looks frightening in isolation can be rational once you see the

asset it bought and the revenue it is producing. The bill for the AI buildout is

coming due. Next week, we will start to find out who can pay for it.

Trade accordingly.

The views expressed by Lance Roberts are not

necessarily those of RetireEarlyLifestyle.com

Billy and Akaisha Kaderli are

recognized retirement experts and internationally published authors on

topics of finance, medical tourism and world travel. With the wealth of

information they share on their award winning website RetireEarlyLifestyle.com,

they have been helping people achieve their own retirement dreams since

1991. They wrote the popular books, The

Adventurer’s Guide to Early Retirement and Your

Retirement Dream IS Possible available on their website

bookstore or

on Amazon.com.

Retire

Early Lifestyle appeals to a different

kind of person – the person who prizes their

independence, values their

time, and who doesn’t want to mindlessly

follow the crowd.